Free Cash Flow, Amazon, and the Teleportation Business

Jan 20 · 10 min

TL;DR — In his 2004 annual letter (1), Jeff Bezos, the entrepreneurial genius who founded Amazon in 1994, describes a hypothetical teleportation business to illustrate the advantages of using free cash flow, instead of earnings, to analyze investments.

Considering only earnings, this teleportation business seems to be a success. However, when analyzing its free cash flow, it appears to be "fundamentally flawed," in Bezos' words. Based on these cash flows, Bezos concludes that the teleportation business is not viable.

Why is there a difference between earnings and free cash flow? We will see here that there is no such difference, and that the teleportation business, as formulated by Bezos, is absolutely viable.

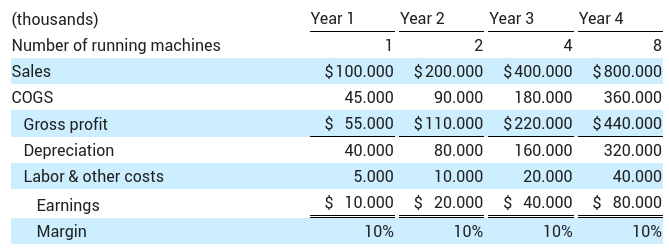

Let's start by describing the business proposed by Bezos. A startup develops a machine capable of teleporting people. Each machine costs $160 million to build and can serve 100,000 (brave) travelers a year. These brave travelers must have some purchasing power, as each trip sells for $1,000.

Since the time savings are considerable compared to traditional travel, all the machines we build will be fully utilized, resulting in revenue of $100 million per machine per year. In terms of expenses, each trip costs $450 in materials and energy and $50 in personnel and other costs.

Every year, the manufacturing process improves, allowing us to build twice as many machines as the year before. Each machine has a four-year lifespan. With this in mind, here is the income statement for this business in its first four years of life.

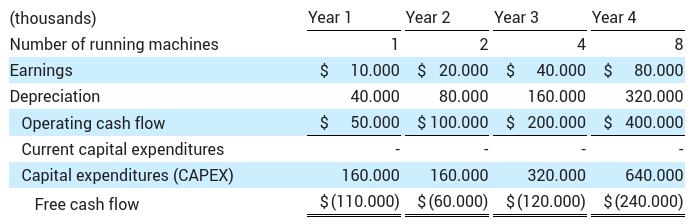

We're making $10 million a year per machine, a 10% net margin. Not bad. So, what's the problem with the business that Bezos describes in his letter? The problem he sees is not in the $10 million of earnings but in the average free cash flow losses of $130 million over these four years.

Here we are calculating free cash flows by adding depreciation to earnings since depreciation is an expense that does not involve any cash outflow from the company, and also by subtracting cash expenses for new investments in current capital (which we do not have here) and in fixed assets, or CAPEX (for the construction of each machine).

Bezos, seeing all these negative cash flows, concludes that the teleportation business is a disaster, that it's "fundamentally flawed."

Which financial statement is closer to the reality of the business, and which one should we use as investors? The one that tells us we are earning $10 million a year? Or the one that tells us we are losing, on average, about $130 million a year?

The next three years

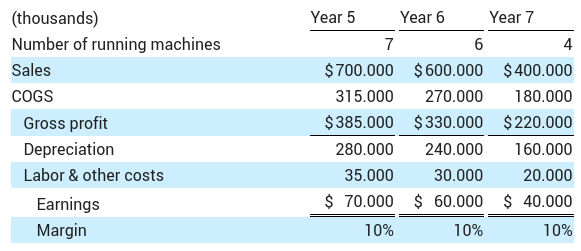

The answer is that both financial statements are telling the "truth" because they are just two different ways of describing the same reality. Let's check it out. Let's pause this "reality" for a moment—that is, let's stop building machines—and extend both statements for three more years.

In the income statement, there is not much difference. We are still earning $10 million per year per machine, with a 10% net margin, for a total of $320 million over those seven years.

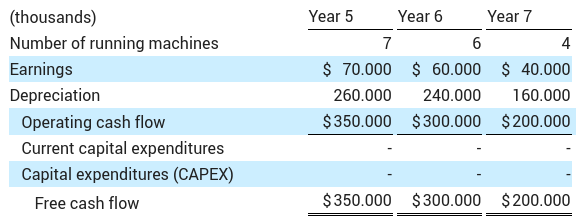

But in the free cash flow statement, we see a change from the fifth year onwards. There is now a free cash inflow. In those three additional years, the cash losses of the first four years are reversed because we have stopped building new machines and are just monetizing the ones already available. Adding up the free cash flows over all seven years, we have a total inflow of $320 million.

Bezos states that "the duality between earnings and cash flows comes up all the time." There is no such duality. Both financial statements ultimately agree that we have earned $320 million. They are just different lenses through which to view the same reality, and when we look at the full reality through both lenses, we see the same thing.

The two statements differ only when we see a small part of reality, such as a single accounting period. But the more accounting periods we look at, the more of this "reality" we see, and the closer the two figures will become. By definition, they must eventually converge.

So, what do we do as investors? Which financial statement do we use? Well, it depends. It depends on the period of reality that we have at our disposal to observe.

If we only have a small number of accounting periods (one, two, or three), the income statement and the earnings figure will give us a more accurate picture of the whole reality (not just that of those periods). On the other hand, the free cash flow will give us a more faithful image of those specific periods, but not of the whole reality.

If the number of periods is large enough (more than seven), it doesn't matter which statement we use.

From theory to practice

If we could look at just one period, the earnings from that period would bring us closer to the company's reality than the free cash flow. This is the objective of the "accrual method" of accounting and the matching principle (correlation of income and expenses) on which the income statement is based. The goal is to match each income with its corresponding expense.

We are distributing the huge expense of building each machine over the four years in which it generates income. That way, by looking at just one year, we can see that it is profitable to build the machine and that it is generating a 10% net margin for us.

If we do not match revenues and expenses and instead consider only cash receipts and payments, we are using the "cash method" of accounting. With this method, we see huge machine construction costs in the first four years, which become profitable over the following three years when we stop building new machines and simply collect the free cash flows they generate.

Up to this point, the accrual method of matching income and expenses may seem better because, regardless of the number of periods we observe, the accounting will always be close to the company's reality. This is why the most important international accounting bodies (FASB and IASB) stipulate that annual accounts must be prepared using the accrual method.

But the accrual method has one great, very important disadvantage: to make a few accounting periods reflect the company's reality, it is necessary to make many estimates. Accounting standards allow some freedom in setting those estimates (for example, the number of periods over which to distribute our machine expenses). This freedom is good because it allows companies to bring their accounts closer to their reality. On the other hand, it also allows a certain flexibility in adjusting account balances, especially the earnings figure, to the value that management wants stakeholders to see. This flexibility does not exist, or exists to a lesser extent, with the cash method and free cash flow figures.

What to use then for investment decision making

We should almost certainly use free cash flows and a sufficiently large number of periods (at least seven). In our example, the earnings and free cash flow figures are equivalent because we made the correct estimates for calculating earnings. But in the real world, those estimates (which are more complex than in our case) are sometimes forced or even abused to show an earnings figure that, for example, allows management to obtain certain year-end bonuses or causes the stock to go up temporarily.

According to Trevor Harris, a former vice president at Morgan Stanley, "the financial reporting system is completely broken." Broken by the amount, complexity, and laxity of all the estimates currently allowed by the FASB and IASB.

The article "Fuzzy Numbers" (2) is an excellent account of the abuse of these estimates and how they have been used.

References

(1) Amazon.com 2004 Letter to Shareholders

(2) Henry, David, “Fuzzy Numbers,” Business Week (October 4, 2004)

(3) George C. Christy, Free Cash Flow Statement. John Wiley & Sons, Inc., 2009